The Elements of Innovation Discovered

The Elements of Innovation Discovered

Metal Tech News – August 16, 2023

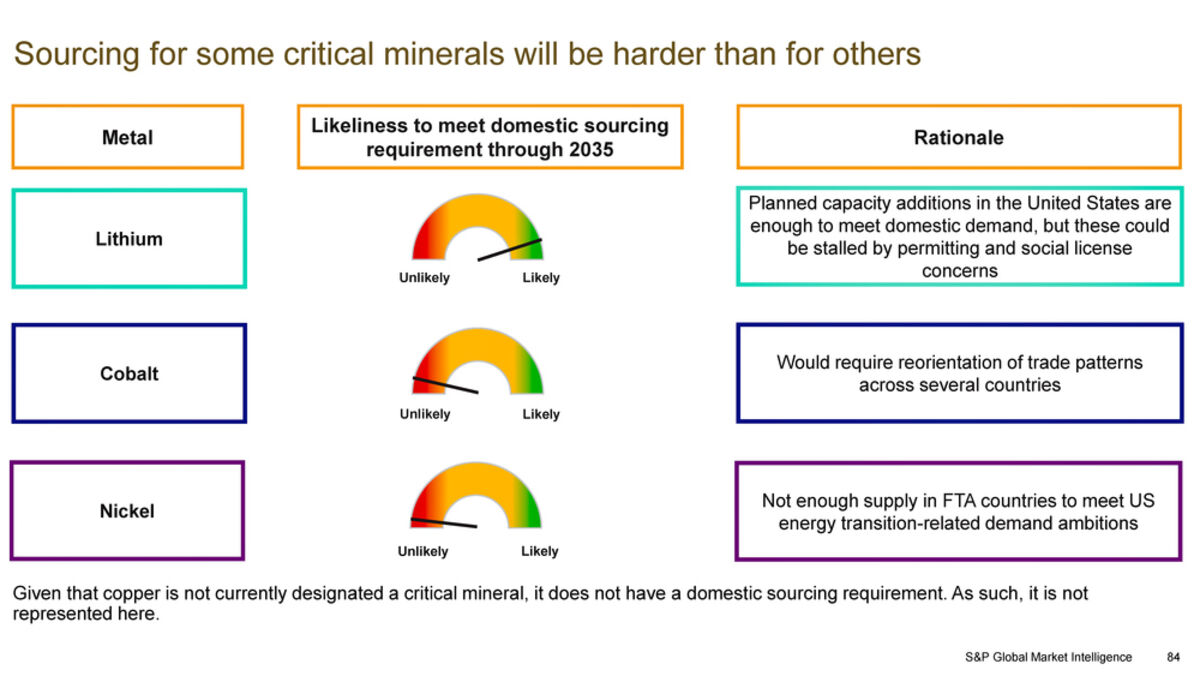

S&P Global analysts forecast the U.S. will likely have adequate supplies of lithium that meets Inflation Reduction Act sourcing requirements but not enough cobalt or nickel.

S&P Global study details enormous energy transition metals demand in the US; significant supply challenges at home, abroad.

The United States has "considerable challenges" to overcome when it comes to securing enough critical minerals and copper to meet the increased energy transition-related demands being driven by the Inflation Reduction Act, according to analysis by S&P Global.

Detailed in a ne...

Reader Comments(0)