The Elements of Innovation Discovered

The Elements of Innovation Discovered

Metal Tech News - May 23, 2025

IEA underscores critical minerals as a frontline issue in safeguarding global energy and economic security.

IEA is forecasting a 10% copper supply deficit by 2035.

Oversupply forced BHP to shut down Nickel West, one of the most sustainable sources of battery-grade nickel.

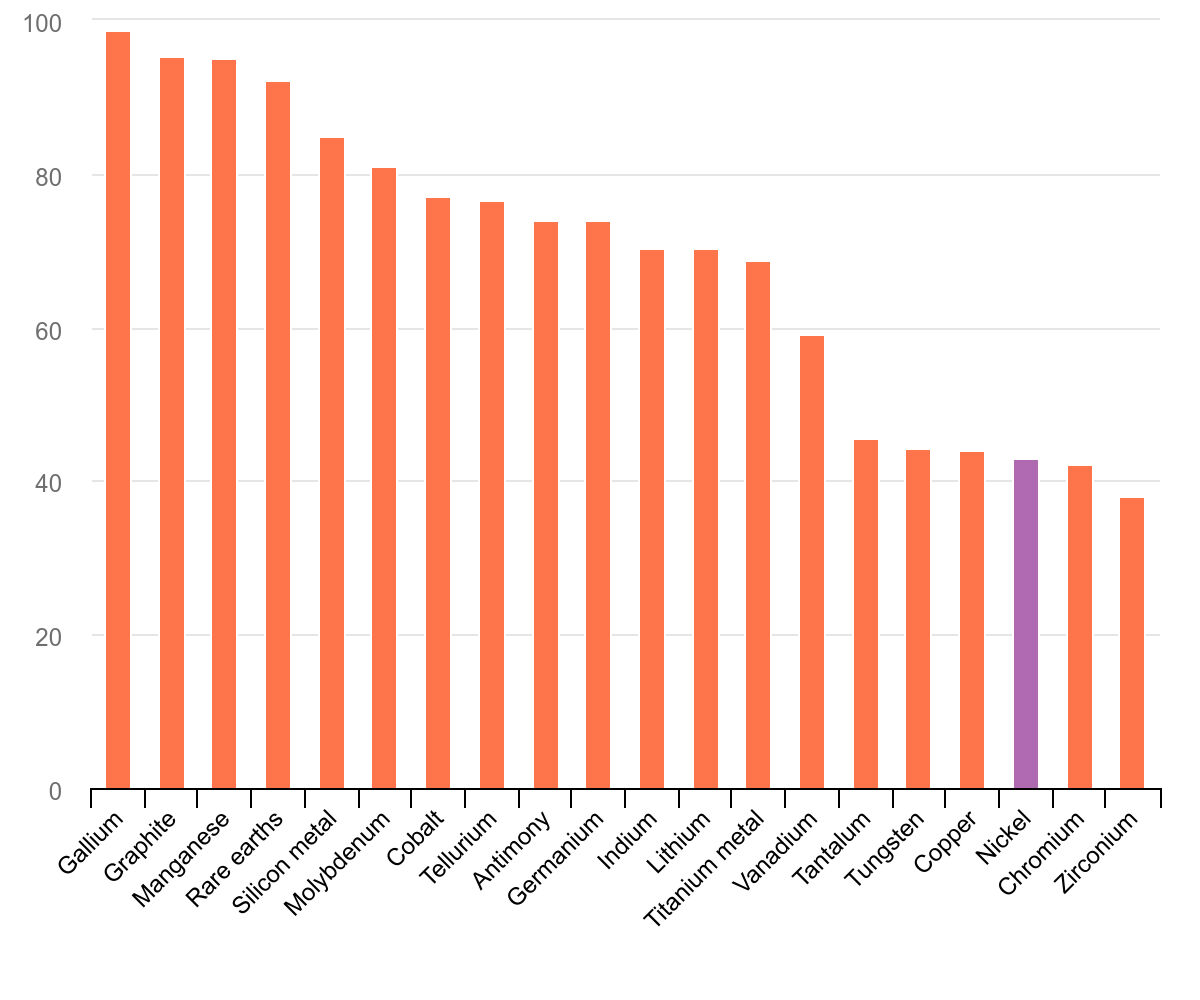

China is the top refiner of 19 out of 20 energy minerals.

Even as Western governments ramp up efforts to secure critical mineral supply chains, the International Energy Agency warns that global dependency on a few nations – primarily China – is growing. This tightening grip poses heightened risks to energy security, industrial competitiveness, and clean energy ambitions.

"In a world of high geopolitical tensions, critical minerals have emerged as a frontline issue in safeguarding global energy and economic security," International Energy Agency Executive Director Fatih Birol said in a statement introducing the agency's 2025 critical minerals report.

China is the top refiner of 19 out of 20 energy minerals.

Titled "Diversification is the cornerstone of energy security, yet critical minerals are moving in the opposite direction," the new report finds that three countries control 86% of the world's supply of copper, cobalt, graphite, lithium, nickel, and rare earth elements. This is higher than the 82% control the top three nations held in 2020, when the pandemic awakened Western policymakers to the risks of concentrated supply chains.

The supply chains for all the energy metals highlighted in the IEA report lead to China, the world's top supplier of five of them. The one exception, nickel, is primarily supplied by Indonesia with Chinese support.

"This new analysis reviews what is at stake and what needs to be done to improve the resilience and diversity of critical mineral supply chains – a key concern for ensuring the reliability, affordability, and sustainability of energy in the 21st century," said Birol.

China's leveraging its control over critical mineral supply chains as a geopolitical power play has made the stakes clear to policymakers and military leaders in the West.

"Recent disruptions [due to] adversarial actions have underscored what we have long recognized, that it is more urgent than ever to build capability and resilience in supply chains for critical minerals," Adam Burstein, a technical director for strategic and critical materials at the Pentagon, said during an address earlier this year at the Naval War College in Rhode Island.

The disruptions referred to by Burstein are the restrictions and bans that China has placed on the exports of 16 critical minerals and metals.

Oversupply forced BHP to shut down Nickel West, one of the most sustainable sources of battery-grade nickel.

At the other end of the spectrum, China and Indonesia have overproduced and oversupplied the market with many of the minerals and metals critical to the energy transition – forcing out competition due to driving down prices to a point where projects operated under Western environmental and labor laws are no longer economic.

China-backed overproduction from Indonesia has flooded global markets with low-cost nickel, displacing higher-standard competitors. This price war contributed to BHP's 2024 decision to suspend operations at its Nickel West mine in Western Australia.

IEA cautions that an oversaturated energy metals market does not eliminate the supply risks associated with narrow supply chains.

"Even in a well-supplied market, critical mineral supply chains can be highly vulnerable to supply shocks, be they from extreme weather, a technical failure, or trade disruptions," Birol said. "The impact of a supply shock can be far-reaching, bringing higher prices for consumers and reducing industrial competitiveness."

Without forward-thinking and risk-taking investors, mining companies, and policymakers in the West, China could continue to consolidate its control over critical mineral markets as the energy transition unfolds.

Driven by its increased use in the batteries powering electric vehicles and storing renewable energy, the demand for lithium rocketed 30% in 2024. At the same time, the demand for nickel, cobalt, graphite, and rare earths increased by 6‑8% in 2024.

IEA expects demand growth to continue for at least another 15 years. Based on current climate targets and technologies, the agency anticipates a fivefold growth in lithium demand by 2040. Over that same span, the demand for graphite and nickel is expected to double, and the demand for cobalt and rare earths increase by more than 50%.

IEA is forecasting a 10% copper supply deficit by 2035.

Even the demand for copper, an already widely used metal with a large market, is expected to increase by 30% over the next 15 years.

In fact, copper is an energy metal IEA is particularly concerned about – forecasting a 30% supply deficit by 2035.

However, investment in the exploration and development of all energy metals has been lackluster in comparison to demand projections.

"Investment momentum in critical minerals has weakened: spending grew by just 5% in 2024, down from an increase of 14% in 2023. Exploration activity plateaued in 2024, marking a pause in the upward trend seen since 2020, and start-up funding showed signs of a slowdown," IEA penned in its report.

This has opened up the opportunity for China to gain a tighter grip on energy mineral supply chains. China and Indonesia accounted for roughly 90% of the 2024 supply growth for cobalt, graphite, nickel, and rare earths, according to the IEA.

While IEA foresees some diversification of lithium, graphite, and rare earth supply chains, the agency expects China, through its connections in Indonesia and Africa, to further solidify its control over the global supply of copper, nickel, and cobalt.

This concentration of supply leaves the demand end of global critical mineral supply chains at risk – not only from pandemics or natural disasters breaking a link, but from suppliers that leverage their dominance for geopolitical gain and to consolidate manufacturing in a location where there is a plentiful and reliable supply of the elemental building blocks of high-tech and clean energy. Today, and for the foreseeable future, that place is China.

CORRECTION: This article was corrected on June 1 to accurately report IEA's forecasted 2035 copper supply deficit at 30%.

With more than 17 years of covering mining, Shane is renowned for his insights and in-depth analysis of mining, mineral exploration, and technology metals.

Reader Comments(0)