The Elements of Innovation Discovered

The Elements of Innovation Discovered

Critical Minerals Alliances - August 7, 2025

Developing secure and sustainable lithium supply chains has become a strategic imperative impacting climate policy, national security, and industry competitiveness.

The Salton Sea geothermal field in Southern California offers the U.S. an abundance of clean electricity and lithium for the energy transition.

Smackover Lithium, ExxonMobil, Albemarle, and Occidental are among the companies developing projects to extract lithium from the Smackover Formation under southern Arkansas.

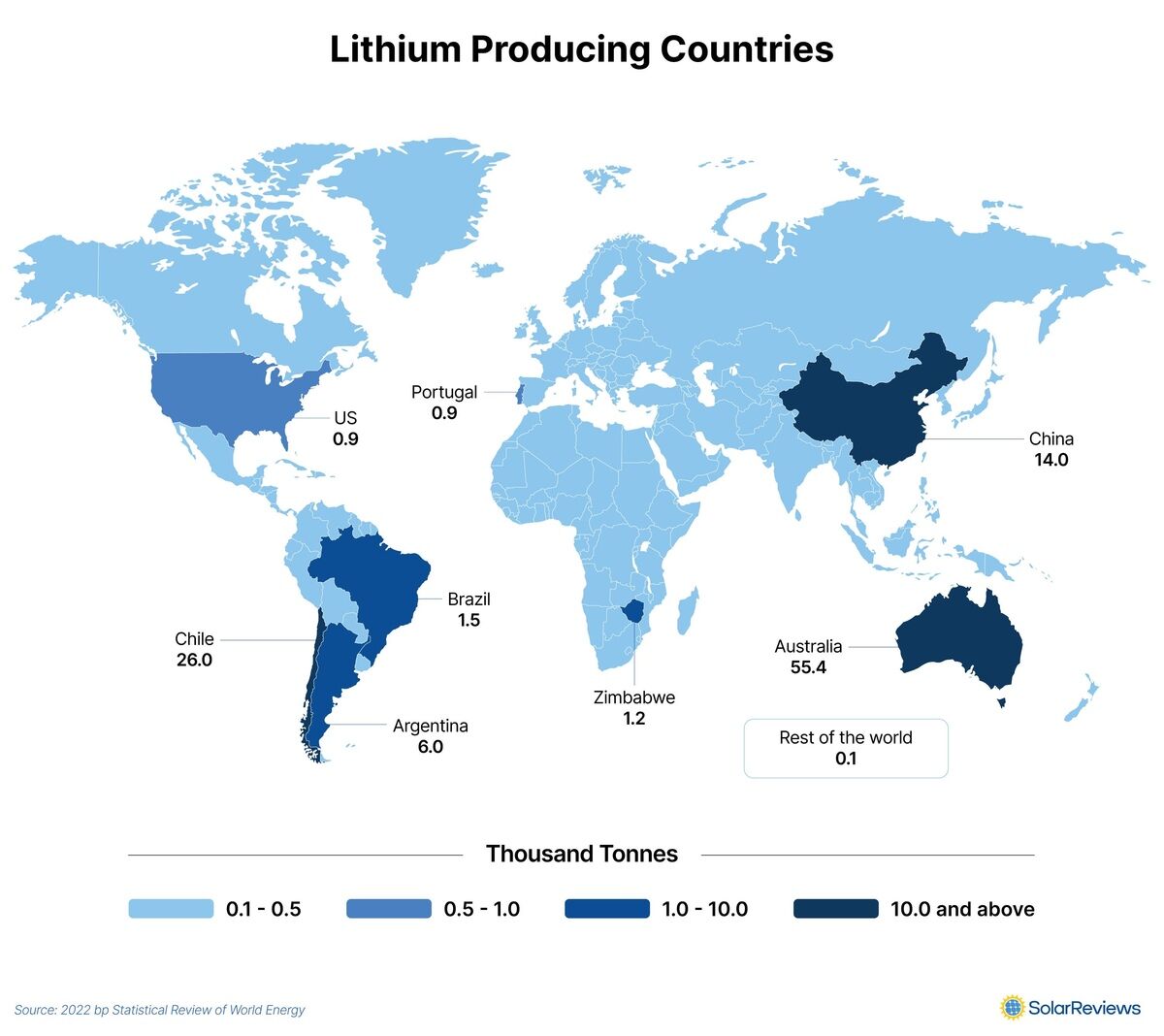

After lithium prices plummeted to four-year lows in 2024, this year may mark either a turning point or a series of course corrections for the critical mineral powering global energy storage.

Stabilizing prices and rising demand from green tech signal a shifting landscape marked by technological disruption, regulatory reforms, and intensifying geopolitical competition.

As the namesake metal in the batteries powering electric vehicles and stabilizing electrical grids that are increasingly being fed intermittent renewable energy, lithium has become central to global clean energy ambitions. As countries work to meet decarbonization targets, the establishment of secure and sustainable lithium supply chains has become a strategic imperative impacting climate policy, national security, and industry competitiveness.

While lithium prices have been suppressed by new supply outpacing demand, slow recovery is now underway. Strong EV sales in China and strategic mine suspensions in Australia – such as Bald Hill and Mt. Cattlin – have helped rebalance supply. However, analysts warn the rebound is fragile. High-cost projects like Greenbushes, Wodgina, and Pilgangoora remain inactive but could quickly restart.

"This swing supply dynamic could serve as a cap on price increases in 2025, as rapid restarts may lead to a more oversupplied market than currently forecast," said Federico Gay, principal lithium analyst at industry consultancy Benchmark Mineral Intelligence.

But these aren't fallow cornfields taking a respite from overproducing – it is far from cheap to leave a mine sitting idle.

"Operations that are producing at a reduced utilization rate could, however, restart in as little as a month," said Thomas Matthews, analyst at CRU Group, citing the temporary shutdowns and scaled-back production in Australia. "The market balance will be dependent on whether we see these operations ramping up, or whether more supply will be curtailed."

Both the hesitation to reduce supply and the potential to jump the gun and resume production prematurely stem from a majority of forecasts that promise demand will increase significantly in the longer term as the energy transition progresses.

Geopolitical tensions and tariff uncertainty may drive miners to continue extraction amid fears of markets fracturing into competing trade blocs. The intensifying rivalry between China and the West has been driving fragmentation in the world's economic order, with emerging political and economic shifts between countries seeking to build stronger relationships and trade advantages within their own sphere of influence.

The International Energy Agency (IEA) Global Critical Minerals Outlook 2025 finds that critical mineral markets have become more concentrated, not less, particularly when it comes to refining and processing.

"Even in a well-supplied market, critical mineral supply chains can be highly vulnerable to supply shocks, be they from extreme weather, a technical failure or trade disruptions," said IEA Executive Director Fatih Birol. "The impact of a supply shock can be far-reaching, bringing higher prices for consumers and reducing industrial competitiveness."

Meanwhile, solid-state and silicon-anode batteries are reshaping lithium demand by offering safer, higher-density, and faster-charging alternatives. These innovations reduce the use of metals like cobalt and nickel while expanding applications in aerospace, electronics, and grid storage, thereby decreasing the lithium required per product while also broadening its offerings.

In 2023, automakers made bold moves to secure raw materials for the EV transition. General Motors invested $650 million in Lithium Americas' Thacker Pass project in Nevada, while Ford inked offtake deals with major suppliers, including Albemarle, the world's largest lithium producer.

Lithium prices tumbled in early 2024, falling below $14,000 per metric ton, down more than 80% from 2022 highs, due to oversupply, slower EV adoption, and investor caution.

Albemarle responded by cutting jobs and delaying key projects in the Carolinas, including what would have been the nation's largest lithium refinery. Piedmont Lithium Inc. canceled plans for a Tennessee processing plant and declined a $142 million federal grant, instead focusing on its North Carolina assets. GM postponed further funding for Thacker Pass.

Meanwhile, partnerships aimed at diversifying lithium supply gained traction.

In June 2024, SK On signed a memorandum of understanding with ExxonMobil to source up to 100,000 metric tons annually from Exxon's Project Evergreen in Arkansas, supporting its U.S. battery plants. ExxonMobil later signed a similar deal with LG Chem.

By April, Thacker Pass was back on track, bolstered by a $250 million Orion Partners investment and a $2.26 billion loan from the U.S. Department of Energy. The site aims to produce 40,000 metric tons per year of battery-grade lithium carbonate.

By midyear, lithium prices stabilized with a rebound in Chinese demand and reduced Australian output. However, cautious U.S. producers continued to scale back expansion plans, including Albemarle's cancellation of a $1.3 billion refinery in South Carolina, citing poor economics.

"We've been wanting to build this Western supply chain. The economics just aren't there to build that plant out in South Carolina," said Albemarle CEO Kent Masters. "We don't have the confidence to say where (the lithium price) is or where it's going ... I don't think private companies are going to be able to do it on their own."

The largest U.S. lithium resources lie in Nevada's hard rock and claystone deposits, the Smackover Formation under southern Arkansas, the Salton Sea's geothermal brines in California, and spodumene in North Carolina. But American producers remain at a cost disadvantage to China's state-supported supply chain.

To build out its own supply chain, the U.S. is streamlining the permitting of lithium exploration, mining, and processing projects.

Jindalee Lithium's McDermitt lithium exploration project on the Oregon-Nevada border and Albemarle's King's Mountain lithium processing plant were the first lithium projects accepted for FAST-41, a federal program to increase transparency, enhance agency coordination, and expedite permitting of large projects in the U.S.

While McDermitt and King's Mountain were added to the FAST-41 Dashboard primarily to provide increased transparency, Controlled Thermal Resources' Hell's Kitchen geothermal brine project in Southern California, which was accepted by the program in June, is the first domestic lithium project to take part in the coordinated and streamlined permitting offered by FAST-41.

"FAST-41 coverage signifies a critical federal recognition of the Hell's Kitchen Project," said Controlled Thermal Resources CEO Rod Colwell. "We have an extraordinary resource and the proven technology to commence construction at scale. We applaud the federal government's decisive and efficient actions to accelerate development, encourage private investment, and create thousands of good-paying American jobs."

2025 has also brought a wave of new battery regulations. Updates to classification, labeling, and transport aim to enhance safety and promote greener chemistries.

Ioneer Ltd. received approval to begin developing the Rhyolite Ridge lithium-boron project in Nevada, which has received a conditional commitment of up to $700 million from DOE and a supply agreement with Ford and backing from Sibanye-Stillwater.

American Battery Technology Company (ABTC), part of a group of players integrating production with domestic lithium supply, is advancing a lithium extraction and processing facility in Nevada, focusing on claystone resources.

The project has garnered substantial support, including a $900 million letter of interest from the Export-Import Bank of the United States, which aims to help establish a full-cycle domestic supply of battery-grade lithium through mining and recycling.

Smackover Lithium, ExxonMobil, Albemarle, and Occidental are among the companies developing projects to extract lithium from the Smackover Formation under southern Arkansas.

In 1905, a breach in the Colorado River filled a dry lakebed in Southern California, creating the Salton Sea. Once a popular destination, the lake became increasingly saline and toxic as inflow declined. What remains are mineral-rich geothermal brines with concentrations of lithium beneath the lake's southeastern edge.

The Salton Sea Geothermal Field contains an estimated 2,950 megawatts of geothermal potential and is considered one of the richest lithium brine resources in North America. This pairing supports simultaneous production of renewable energy and battery-grade lithium.

Controlled Thermal Resources' $1.8 billion Hell's Kitchen project leads development in the region, targeting up to 300,000 metric tons of lithium annually. Partners include Fuji Electric, Stellantis, and General Motors, which has committed $650 million to secure priority access to CTR's U.S.-produced lithium.

Berkshire Hathaway Energy is piloting lithium recovery at its 10 geothermal plants in the region, with support from the U.S. Department of Energy. EnergySource Minerals is developing its ATLiS project to extract lithium, silica, and zinc using direct lithium extraction (DLE). Lilac Solutions, backed by Breakthrough Energy and other private investors, is also active in the region, working with developers to scale DLE technologies.

DLE methods are designed to accelerate recovery while minimizing water use and surface disturbance compared to traditional evaporation ponds or hard rock mining.

Beyond California, the Smackover Formation is a lithium-rich geological formation spanning Arkansas, Texas, Louisiana, Mississippi, Alabama, and Florida. Estimated resources range from 5 to 19 million tons – enough for hundreds of millions of electric vehicle batteries.

Smackover Lithium, a joint venture between Standard Lithium (55%) and Equinor (45%), received a $225 million DOE grant and aims to produce enough lithium to support approximately 900,000 EVs per year from Arkansas brines.

Stardust Power is constructing a lithium refinery in Oklahoma to process concentrate from Smackover brines. The company has signed a purchase agreement with Japan's Sumitomo Corporation for 20,000 metric tons of lithium carbonate per year.

Other companies developing Smackover brine projects include ExxonMobil, Chevron, Albemarle, Occidental, Lanxess, and Tetra Technologies.

The Salton Sea geothermal field in Southern California offers the U.S. an abundance of clean electricity and lithium for the energy transition.

Due to the environmental challenges of lithium processing and its status as both highly demanded and geologically scarce, several emerging battery technologies are being developed to reduce reliance on this lightest metal on the periodic table.

Among the most promising are sodium-ion batteries, which replace lithium with more abundant and geopolitically neutral sodium. These batteries are especially attractive for grid-scale energy storage and entry-level EVs, where cost and safety take precedence over energy density.

Chinese battery giants like CATL and BYD have already begun deploying sodium-ion batteries in electric scooters and compact vehicles, while hybrid sodium-lithium chemistries are being piloted for broader automotive applications. The European Union is also investing in sodium-ion research and development as part of its broader battery innovation programs.

Though sodium-ion cells currently lag in energy density, advances in cathode design, hybrid battery systems, and ultracapacitors are narrowing that gap – and if commercial deployment scales, they could significantly reduce global lithium dependency over the next decade.

Manufacturers are also ramping up production of lithium iron phosphate (LFP) and lithium manganese iron phosphate (LMFP) batteries, which require less lithium than high-nickel chemistries while offering high thermal stability and lower cost. Automakers like Tesla, BYD, Ford, and General Motors are adopting these chemistries for both cost savings and supply chain diversification.

Solid-state battery research, which may ultimately reduce or replace the use of lithium entirely, continues to gain momentum.

Meanwhile, Talon Metals and Argonne National Laboratory are collaborating to convert iron-rich waste from nickel mining into LFP cathode materials, demonstrating growing interest in circular economy strategies and integrated resource recovery for critical materials.

Despite emerging alternatives, lithium remains the backbone of electrification. With China's refining dominance and rising resource nationalism, control over lithium is now a matter of strategic autonomy.

In the end, this linchpin to clean energy storage is being pulled in every direction: toward the economy, toward security, and sustainability. How the world balances those forces in the years ahead will determine whether the lithium industry can keep pace with the ambitions it now underwrites.

Reader Comments(0)