The Elements of Innovation Discovered

The Elements of Innovation Discovered

Critical Minerals Alliances - August 7, 2025

As the U.S. redefines its global resource strategy, a growing network of allied partnerships aims to shift mineral access away from single-source dependence.

As mineral trade routes evolve, the global logistics landscape is adjusting to new alignments in supply, demand, and strategic access.

Gracelin Baskaran

As the United States moves to loosen China's grip on critical mineral supply chains, nations across Africa, the Arctic, the Americas, and the Indo-Pacific are emerging as potential partners in a broader strategy to secure resources and strengthen domestic production. While not all deals are finalized, diplomatic outreach, technical dialogues, and preliminary investment proposals signal Washington's intent to build resilient, allied supply chains and reduce reliance on rivals.

The search for secure mineral supply has pushed the U.S. to explore a wider field of potential partners, each offering resources vital to clean energy, defense, and advanced manufacturing.

A growing number of Arctic, Baltic, Middle Eastern, African, Asian, and South Pacific nations are joining a layered strategy to diversify sourcing and reduce reliance on Chinese-controlled supply chains.

The nations now under Washington's focus offer specific resources essential to U.S. priorities: rare earth elements and uranium from Greenland; cobalt, copper, and tantalum from the Democratic Republic of Congo; manganese from Botswana; rare earths from Namibia; nickel and cobalt from Indonesia; and additional regional contributions such as Rwanda's potential role in a broader minerals-for-security framework alongside the DRC.

These engagements differ in structure and progress – some driven by draft proposals or investment commitments, others by technical studies or strategic dialogues – but all aim to secure critical inputs for clean energy, manufacturing, and defense while limiting exposure to Chinese-dominated supply chains.

Of the few partnerships that have advanced beyond preliminary assurances, the agreement with Ukraine provides a model of how the U.S. aims to align critical mineral development with broader economic and security objectives.

Finalized in early 2025, the accord established a joint investment fund to support Ukraine's reconstruction, backed by future revenues from mineral and hydrocarbon projects, while also securing U.S. involvement in developing untapped resources like lithium, graphite, and rare earths.

A more in-depth look at the landmark agreement between the United States and Ukraine can be found in the "Historic U.S.-Ukraine minerals accord" article on Page 51 of Critical Minerals Alliances 2025.

Similarly, partnerships with Saudi Arabia and the United Arab Emirates reflect how U.S. strategy combines government-level accords with large-scale commercial deals to secure critical resources and expand refining and processing capacity within allied jurisdictions.

These arrangements, established shortly after the Ukraine deal, are positioned to support regional supply chains while advancing shared goals of industrial diversification and energy transition.

A detailed analysis of U.S. partnerships with Saudi Arabia and the United Arab Emirates is available in the "U.S. charts critical future with Middle East" article on Page 48 of Critical Minerals Alliances 2025.

Together, these evolving relationships – whether in negotiations or already formalized – illustrate how the U.S. is working to transform early-stage diplomacy and commercial outreach into a resilient network of mineral partnerships.

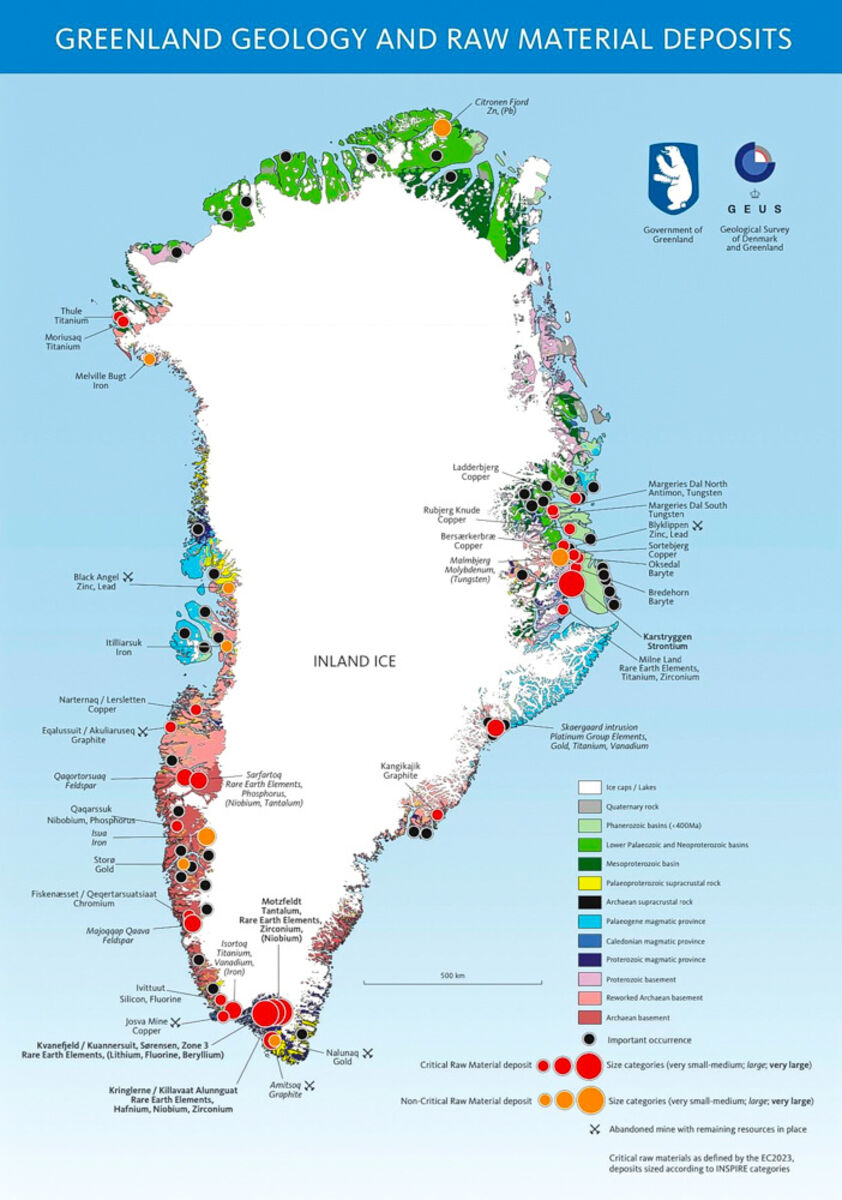

Rich in critical minerals essential to clean energy, manufacturing, and defense, Greenland has emerged as a pivotal node in Western efforts to secure strategic resources and reduce reliance on Chinese-controlled supply chains.

Holding 25 of the 34 minerals designated as critical by the European Union and 20 of the 50 listed by the U.S., including rare earth elements, uranium, zinc, graphite, and nickel, Greenland's geological endowment aligns closely with allied priorities in supply chain diversification.

Greenland has long held strategic value due to its proximity to Arctic sea lanes and the U.S. Air Force's Thule base, but global headlines surged in 2019 when President Donald Trump proposed buying the island from Denmark – a move quickly dismissed by both Copenhagen and Nuuk.

The episode nonetheless reframed Greenland's geopolitical role, spotlighting its resource potential, military significance, and the risks of Arctic militarization and Chinese mineral influence.

After a period of limited diplomatic reengagement – including the reopening of the U.S. consulate in Nuuk – Greenland returned to the front page in early 2025 when Trump renewed his acquisition proposal.

Danish Prime Minister Mette Frederiksen reaffirmed Greenland's sovereignty while acknowledging the Arctic's growing relevance to defense and economic cooperation. Greenlandic Prime Minister Múte Egede also rejected the sale but expressed willingness to pursue resource partnerships that respect self-rule and deliver local benefits. This stance has attracted interest from both government institutions and private developers seeking to align mineral projects with broader security and supply chain goals.

Among the most advanced efforts is the Tanbreez rare earth project near Narsaq in southern Greenland. Acquired by Nasdaq-listed Critical Metals Corp., Tanbreez is estimated to contain over 4 billion metric tons of ore, including a high proportion of heavy rare earths – critical inputs for defense and magnet technologies that remain difficult to source outside of China.

Further north, the Citronen Fjord zinc-lead project, held by Ironbark Zinc Ltd., ranks among the world's largest undeveloped deposits of its kind. With permits secured and tidewater access available, Citronen has been reviewed by the U.S. Export-Import Bank for potential financing in support of upstream production tied to national security interests.

In the graphite sector, the Amitsoq deposit in South Greenland, being advanced by GreenRoc Strategic Minerals Plc, ranks among the highest-grade graphite projects globally, with measured and indicated grades exceeding 20%.

A 2024 feasibility study outlined an underground mine and processing facility targeting 76,000 metric tons of annual concentrate over a 22-year life. The Export and Investment Fund of Denmark issued a letter of interest to support the project, signaling a more proactive Danish role in securing graphite for European battery supply chains.

Additional activity includes exploration by Anglo American plc under a multi-year license in western Greenland, and continued advancement of the Disko-Nuussuaq project by London-listed 80 Mile plc – a polymetallic system hosting nickel, copper, platinum-group metals, and cobalt.

Despite the scope of Greenland's resource base, development remains constrained by harsh Arctic conditions, limited transportation infrastructure, and complex logistics.

Environmental standards, Indigenous rights, and community benefit agreements impose further conditions on development, requiring projects to meet high thresholds for social and environmental governance.

Still, as Western governments pursue transparent, secure mineral sourcing strategies, Greenland stands out for its stability, alignment with allied interests, and resource diversity. While not easily developed, its mineral wealth and strategic location ensure it remains a focal point in the long-term effort to build resilient supply chains outside of Chinese control.

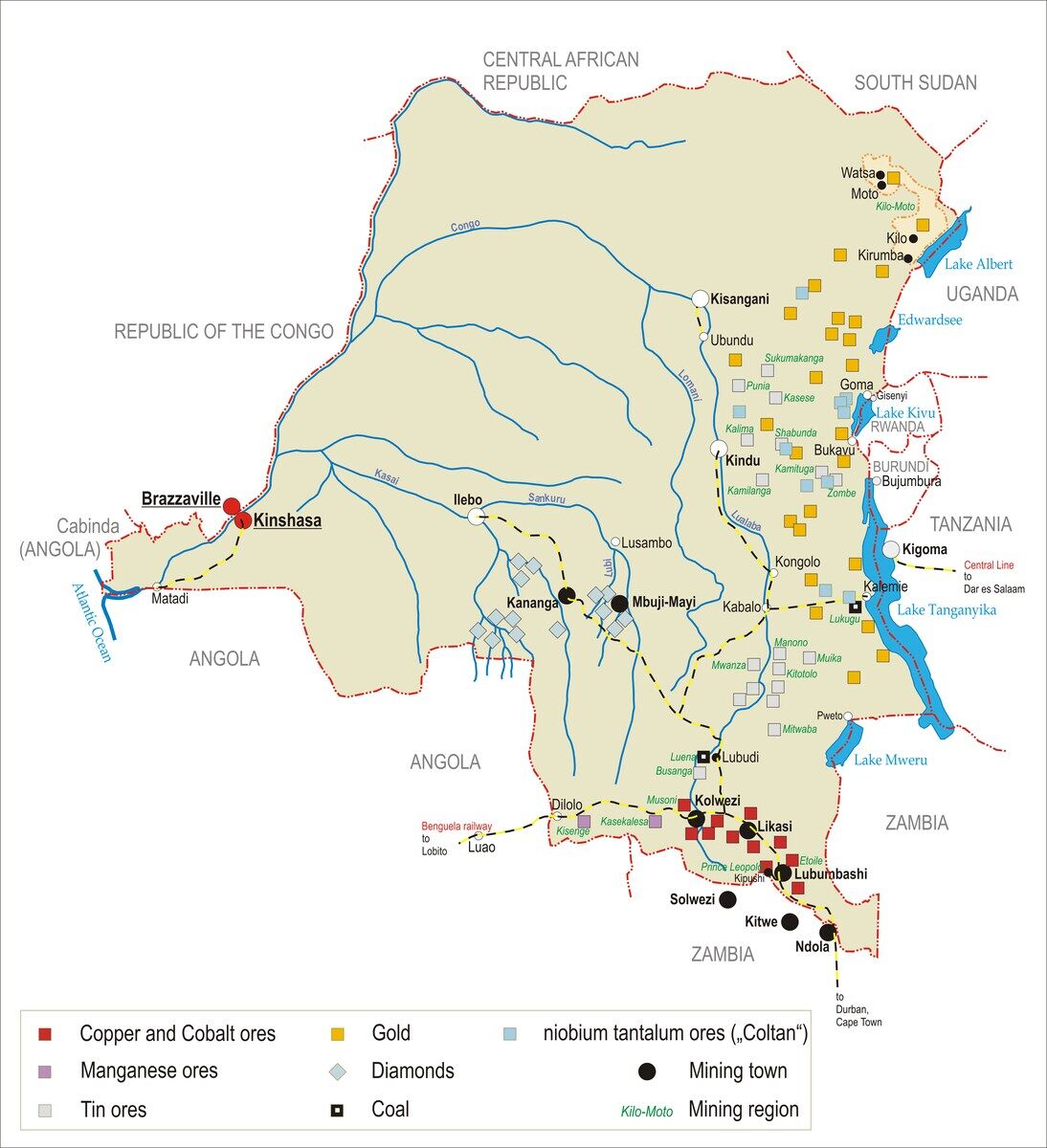

Home to some of the world's richest mineral deposits, the DRC remains indispensable to global clean energy and defense supply chains – yet emblematic of the persistent risks that hinder resource development in high-stakes jurisdictions.

With copper ore grades averaging more than 2.5% – four times the global average – and four of the five largest cobalt mines on Earth located within its borders, the DRC plays a foundational role in battery, electronics, and advanced manufacturing markets.

Exploration investment reached over $130 million in 2024 alone, the highest of any African nation, reinforcing its centrality to the energy transition.

Yet for all its resource wealth, the DRC remains a complex operating environment. Corruption, contract opacity, political instability, and recurring violence have long discouraged Western investment, leaving China to dominate the sector through vertically integrated supply chains backed by state-owned financing and acquisitions.

American engagement has lagged by comparison, despite diplomatic overtures and early-stage efforts to de-risk investment.

Gracelin Baskaran

As Gracelin Baskaran, director of the Critical Minerals Security Program at the Center for Strategic and International Studies, wrote in July, "Transforming diplomatic cooperation into tangible investment in the DRC requires a strategic and sustained effort by the United States ... its complex risk landscape continues to deter private capital."

The latest development came amid escalating conflict in eastern Congo. Following the resurgence of the Rwanda-backed March 23 Movement (M23), Congolese President Félix Tshisekedi proposed granting the United States access to the country's mineral resources in exchange for security assistance.

Originally formed in 2012 and reactivated in 2021, M23 is a rebel group rooted in regional ethnic grievances and failed post-conflict reintegration. Its renewed offensive displaced hundreds of thousands and destabilized key mining regions, particularly in North Kivu and Ituri.

Tshisekedi's proposal catalyzed a new round of shuttle diplomacy in Washington and Doha, where U.S. and Qatari officials helped facilitate dialogue between Congolese and Rwandan delegations.

The resulting peace agreement, signed in Washington in June 2025, aimed to deescalate the M23 crisis and restore stability to mining corridors vital to global cobalt and copper supply.

While mineral access was not formally included in the agreement, the proposal became a foundation for subsequent discussions. Unlike the U.S.-Ukraine accord – where critical mineral revenues were codified into a joint reconstruction fund – U.S. engagement with the DRC remains exploratory, shaped by legacy risks and investor hesitancy.

As U.S. mineral diplomacy expands into new territory, a broader slate of partner nations has entered the fold through preliminary coordination and strategic outreach.

Grouped within this emerging cohort – Botswana, Namibia, Indonesia, Rwanda, and Vietnam – are nations positioned to support allied mineral networks and reduce exposure to Chinese-controlled production and processing.

Leading the charge is Vietnam, advancing negotiations with a pace and magnitude unmatched, and marking the most significant step forward in U.S.-Vietnam relations since 1975. The country's elevation in diplomatic status carries both geopolitical consequences and supply chain potential.

Ranked second globally in rare earth reserves behind China, Vietnam has long represented a dormant opportunity in Western diversification efforts. That opportunity began to take shape with the launch of the U.S.-Vietnam Comprehensive Strategic Partnership in late 2023 – a diplomatic milestone that unlocked a new phase of resource and trade collaboration.

Since then, bilateral efforts have coalesced around rare earth development, with investment dialogues, technical assistance, and joint assessments laying groundwork to bring Vietnamese supply into the allied ecosystem.

In March, the U.S. International Development Finance Corporation signed a memorandum of understanding with Vietnamese mining conglomerate Masan Group Corp. to support rare earth processing.

Though specific terms were not disclosed, the announcement signaled an institutional shift toward concrete cooperation – marking one of the most direct U.S. investment overtures in Southeast Asia's minerals sector to date.

Vietnam's production of rare earth elements increased tenfold between 2021 and 2022, and new targets envision the processing of up to 2 million metric tons of ore and 60,000 metric tons of oxides annually by 2030.

As mineral trade routes evolve, the global logistics landscape is adjusting to new alignments in supply, demand, and strategic access.

While ambitious, these projections align with U.S. efforts to secure permanent magnet supply chains and cut dependence on Chinese-controlled refining.

This push coincides with recent developments in trade. In July, amid negotiations to avoid punitive tariffs on Vietnamese exports, President Trump announced a trade arrangement preserving a 20% rate – lower than expected – while alluding to reciprocal access for American companies and mineral interests.

While not formally codified as a critical minerals agreement, its format reflects a growing trend: tying market access to downstream cooperation on resources, processing, and investment.

At the same time, similar forms of mineral diplomacy are taking shape across other strategic nations. In Botswana, manganese supply discussions remain active; Namibia has advanced its rare earth export capacity with new Western partnerships; and Indonesia's nickel and cobalt sectors remain central to allied battery strategies.

Rwanda, meanwhile, plays a key role in regional coordination alongside the DRC and has participated in U.S.-backed dialogues on supply chain transparency and security.

Together, these emerging relationships illustrate how U.S. mineral strategy is becoming more layered and geographically expansive. Vietnam now anchors that strategy in Southeast Asia – not only because of its resource base, but because of its alignment with broader trade, diplomatic, and security objectives.

In a landscape increasingly defined by supply risk and geopolitical competition, that alignment may prove as important as the minerals themselves.

Reader Comments(0)