The Elements of Innovation Discovered

The Elements of Innovation Discovered

Critical Minerals Alliances - August 7, 2025

General Motors plans to install manganese-rich batteries in Chevrolet Silverado EVs and other electric models by 2028.

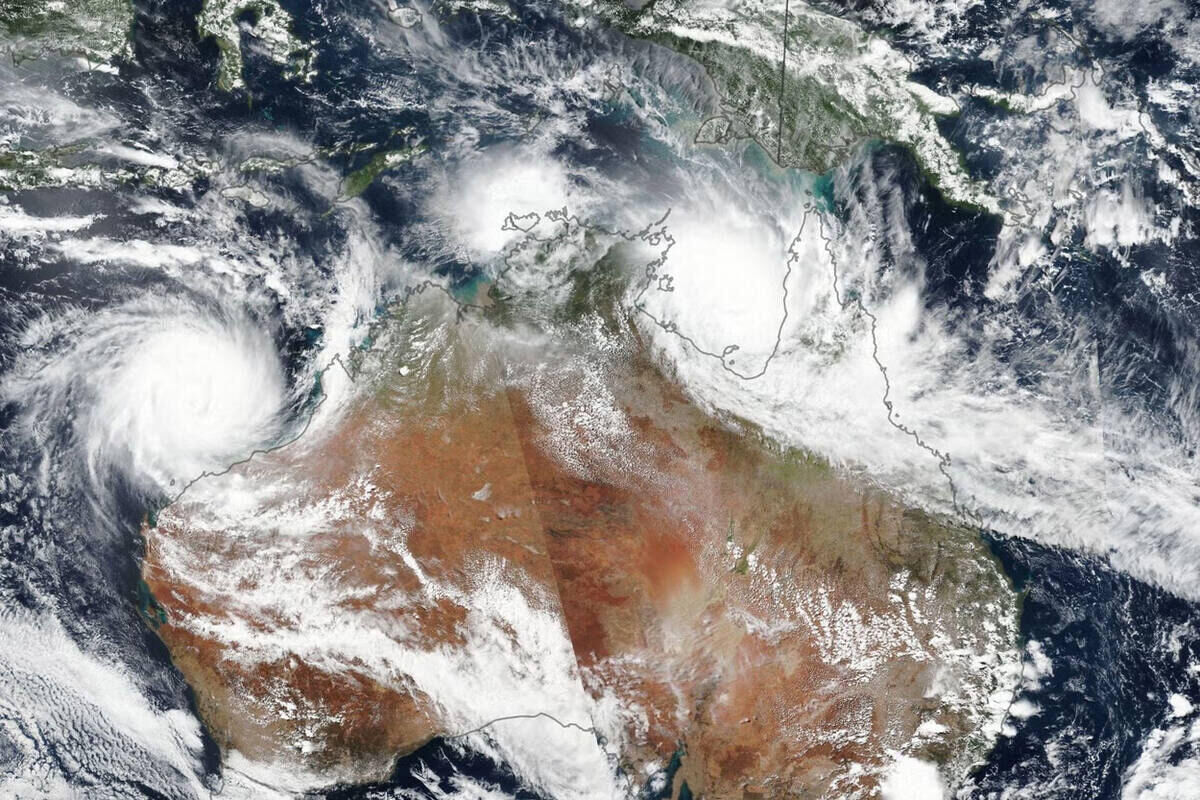

Tropical Cyclone Megan caused significant damage to South32's GEMCO manganese mine in Australia's Northern Territory, driving manganese prices up.

North America is beginning to establish a domestic manganese hub.

Manganese steel, or Hadfield steel, is an alloy with 12-14% manganese. Known for its impact strength and abrasion resistance when hardened.

Humanity has used manganese throughout the centuries in cave paintings, superior Spartan weaponry, potent chemistry, and as a versatile element in manufacturing steel, iron, and several alloys. Today, manganese is gaining recognition as a critical mineral for the clean energy transition. Over the past year, a surge in battery-related demand, geopolitical tensions, and policy support have transformed the manganese market, taking prices on a wild ride.

This transition metal has experienced one of the most volatile pricing years in recent memory, driven by a combination of extreme weather, speculative trading, and shifting demand from China.

The breaking point came in March 2024, when Tropical Cyclone Megan battered South32's Groote Eylandt mine (GEMCO) in Australia – the world's largest manganese producer, which typically supplies around 10% of the world's high-grade manganese. A phased return to mining began three months later, but exports themselves were hindered by flood damage to the local wharf.

With exports offline for over a year, panic set in. Traders and manufacturers rushed to secure supply, driving prices from around $4 to nearly $9 per dry metric ton unit (dmtu) by mid-year. The market overshot, fueled by fears of long-term shortages.

The rally didn't last. As the second half of 2024 unfolded, China's steel sector – the largest consumer of manganese – saw declining demand amid a cooling real estate market and weak infrastructure investment.

Port inventories ballooned to 6 million metric tons, and with consumption dropping, prices plummeted back below $4/dmtu by October, highlighting just how sensitive manganese pricing has become to supply disruptions and economic sentiment.

South32 officially restarted shipments this year from the rebuilt Groote Eylandt wharf, with the first ship departing in late May, and export volumes are expected to return to normal levels by 2026.

This turbulence underscored the fragility of global manganese supply chains and the strategic importance of new, more geographically diverse projects.

In 2024 and early 2025, demand for battery-grade manganese surged as automakers embraced chemistries like lithium-manganese-iron-phosphate (LMFP) and lithium-manganese-rich (LMR) cathodes.

These formulations reduce reliance on expensive, supply-constrained metals like cobalt and nickel, while offering strong thermal stability and cost savings. General Motors, in partnership with LG Energy Solution, has been leading the way with prismatic LMR cathodes containing up to 70% manganese, delivering roughly 33% more energy density than lithium iron phosphate cells at similar costs.

GM plans to deploy these batteries in models like the Silverado EV and Cadillac Escalade IQ by 2028, offering up to 400 miles of range and slashing pack costs by over $6,000.

"We're pioneering manganese-rich battery technology to unlock premium range and performance at an affordable cost, especially in electric trucks," Kurt Kelty, vice president of battery, propulsion, and sustainability at GM, said in May. "As we look to engineer the ideal battery for each vehicle in our diverse EV portfolio, LMR will complement our high-nickel and iron-phosphate solutions."

Ford is also teasing an advanced LMR technology, targeting integration into long-range, affordable EVs later this decade. These developments signal a strategic shift that could significantly increase global manganese demand and cement the mineral's role in next-generation electric mobility.

"Today marks a pivotal moment in Ford's electrification journey and for the future of electric vehicles," Charles Poon, director of electrified propulsion engineering at Ford posted to LinkedIn in April. "After intense research and development at our state-of-the-art Battery Center of Excellence, Ion Park, I'm thrilled to share that the Ford team is delivering a game-changing battery chemistry: Lithium Manganese Rich (LMR)."

Tropical Cyclone Megan caused significant damage to South32's GEMCO manganese mine in Australia's Northern Territory, driving manganese prices up.

Despite rising demand, Western nations remain heavily dependent on China for battery-grade manganese, with over 90% of global refining still taking place there. This puts EV battery production across Europe and North America vulnerable to economic or geopolitical disruptions.

The urgency of diversification is growing. The March 2025 United States Global Survey World Minerals Outlook warns that "magnesium projects outside China have lost funding or encountered other obstacles, and capacity globally is being idled."

As the latest USGS report was being penned, a wave of new high-purity manganese sulphate projects has emerged, backed by public funding and private investment, while automakers race to secure offtake agreements with non-Chinese producers.

GM signed a deal with Element 25 to supply up to 32,500 metric tons per year of battery‑grade manganese sulfate from a new U.S. facility in Louisiana, with GM providing an $85 million loan to support its construction, sourcing Australian manganese concentrate for North American EVs.

Stellantis is backing a similar initiative, committing to supply 45,000 tons of manganese sulfate over five years and investing $30 million to help fund the same Louisiana processing facility.

The U.S. Department of Defense has supported several high-purity manganese efforts as mission-critical, while the EU launches new international projects focused on refining and recycling. Companies like Euro Manganese in the Czech Republic and Giyani Metals in Botswana are advancing, while U.S. and Canadian developers navigate the permitting and feasibility stages.

Though most of these ventures remain pre-production, stronger policy momentum and more receptive capital markets suggest a long-overdue reshaping of manganese's global footprint.

North America is beginning to establish a domestic manganese hub.

In Canada, Manganese X Energy is advancing its Battery Hill project in New Brunswick, where a promising high-purity manganese carbonate deposit is entering pre-feasibility, even sporting a few early-stage agreements underway with EV manufacturers and OEMs.

While South32's Australian project recovers, its Hermosa project in Arizona was the first mining project to be accepted for the FAST-41 (Fixing America's Surface Transportation Act, Title 41) permitting initiative and is one of the most advanced battery-grade manganese developments in America.

FAST-41 is a U.S. law designed to streamline and expedite federal environmental review and permitting for major infrastructure projects, including those related to clean energy and critical minerals.

South32 aims to bring a dual zinc-manganese mine online at Hermosa by 2027, filling a critical gap in the domestic battery supply chain.

Meanwhile, in Minnesota, Electric Metals' Emily manganese mining project is also moving into pre-feasibility following a preliminary economic assessment that showed strong recovery rates and the potential for underground mining and localized refining.

Manganese steel, or Hadfield steel, is an alloy with 12-14% manganese. Known for its impact strength and abrasion resistance when hardened.

As manganese gained prominence in the battery and steel industries, 2024 saw rising emphasis on sustainability. Recycling initiatives picked up momentum, particularly efforts to recover manganese from spent EV batteries and steel scrap, helping reduce reliance on virgin mining.

At the same time, mining and refining operations came under tighter environmental scrutiny, prompting stricter regulations and forcing companies to prioritize cleaner technologies and community engagement. These developments reflected broader pressures, as producers grappled with balancing economic performance with growing investor expectations around environmental stewardship and social impact.

Looking ahead, the outlook for battery-grade manganese remains strong. The global push toward EVs and advanced battery chemistries continues to drive demand growth. Several new mining and refining projects are expected to come online in 2025, aiming to ease supply constraints.

The path forward carries risks, including regulatory hurdles, financing gaps, and geopolitical instability that affects key producers. Opportunities are also emerging, including the rise of sodium-ion batteries utilizing manganese cathodes, increased interest from emerging markets, and a surge in strategic partnerships aimed at securing future supply.

Manganese is poised to become a cornerstone of the clean energy transition – but only if industry and policy can align to support responsible growth. What was once a background metal in the steel industry has now joined similarly overlooked minerals such as vanadium on the front lines of global energy security. Manganese's role in battery technologies will continue driving rapid changes in how the mineral is produced, refined, and governed.

Reader Comments(0)